Canada in a Changing Global Energy Landscape

PDF: Canada in a Changing Global Energy Landscape

On this page

Executive Summary

Insights

Challenges and Opportunities

Scenarios

Implications for Canada

Conclusion

Annex A: Assumptions

References

Executive Summary

The world’s energy landscape is transforming rapidly as the cost of renewable-based electricity, particularly from wind and solar, declines to become competitive with or lower than the price of electricity generated by fossil fuel and nuclear power plants. Power utilities and companies are increasingly choosing to increase their generating capacity using renewable sources rather than fossil power as the perceived problems of intermittent supply from solar and wind are addressed with better supply and demand management using a combination of integrated smart grids and battery storage. The price of batteries is falling precipitously leading to their application at local and grid-level scales in the power supply system as well as facilitating significant electrification of transportation. The shift to an electricity-dominated global energy mix will be accelerated as decreasing costs combine with increasing government and private sector concerns over climate change, energy security and air pollution, particularly in developing countries where the need for additional energy capacity is greatest. In combination, these drivers could lead to renewable-sourced electricity replacing fossil fuels as the dominant form of primary energy used in the global economy for most industrial, commercial and personal activity.

What is driving change?

- Cost Reduction: many components of a renewable-based electricity system are declining in cost much faster than predicted due to advances in technology, economies of scale and accelerating learning curves as experience with these systems grows.

- Digital Economy: digital systems run on electricity; as the global economy shifts to become increasingly digital, the relative proportion of electricity in global energy use will increase.

- Climate Change and Air Pollution: developing countries are embracing renewable energy to meet their economic and development goals without trading off environmental quality and human health.

Policy Challenges: As the insights interact, what challenges could lie ahead?

- A new electricity-based industrial ecosystem could emerge at a much faster rate than expected, significantly disrupting fossil fuel markets.

- Competition for energy markets of the future could be won by those with the best technologies for renewable energy production, storage and management, rather than by those with deposits of fossil energy.

- Minerals and metals such as lithium and rare earths could replace oil, gas and coal as strategic resources based on their use in the batteries, electronics and photovoltaic cells of the emerging energy ecosystem.

- Global oil demand could peak earlier and decline further and faster than expected with significant impacts on high-cost producers.

- Oil production could significantly outpace demand with resulting downward pressure on prices as producer countries compete to maintain their share of shrinking markets while oil still has value.

- Oil could lose its commodity status as purchasers begin to discriminate between oil suppliers on non-intrinsic qualities such as embodied greenhouse gas emissions and/or other environmental, political or social criteria.

Insights

Insights describe developments taking place now that could create further, highly disruptive change in the future should they strengthen. Insights are selected for their disruptive potential and policy implications.

The primary energy supply of the globe is shifting to electricity

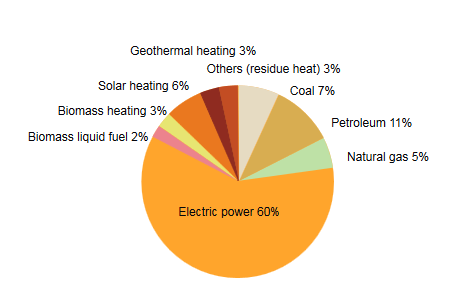

Electricity is expected to be the world’s fastest-growing form of final energy1 and to provide an increasing share of the energy consumed across economic sectors.2 While energy demand from all sources is expected to rise by 37% from 2012-2040,3 over the same period, world electricity demand is expected to increase by almost 80% representing over half of the increase in global primary energy use.4 The emerging middle class in developing countries is expected to drive electrification as it urbanizes and shifts from biomass to electric modern home appliances for cooking, light, heat and cooling. Figure 1 is drawn from a roadmap study by China, the world’s largest economy, demonstrating that it is economically and technically feasible for electricity to comprise over 60% of its end-use energy consumption by 2050.5 The emerging digital economy and related data storage and transmission infrastructure will require increasing amounts of electricity6 as does the growing use of additive manufacturing processes. There are also signals that suggest transportation may electrify more quickly than expected.7

Figure 1: Share of Electricity in End-Use Energy

This image illustrates ‘Share of Electricity in End-Use Energy’ in a pie chart format with electric power at 60%.

Adapted from: China 2050 High Renewable Energy Penetration Scenario and Roadmap Study

Renewable-based electricity is becoming cheaper than generation by fossil fuels

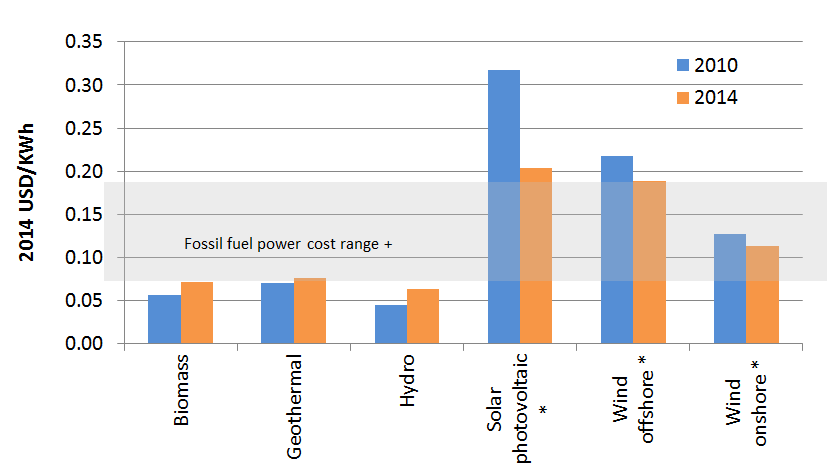

Electricity will be increasingly produced from renewable sources rather than fossil fuels. Rapid advances in renewable energy technology and reductions in cost now permit electricity to be produced relatively inexpensively from a wide range of sources including solar photovoltaics, wind, hydro, geothermal, biomass and biofuels.8 As shown in Figure 2, most renewables can already produce electricity at a lower cost than fossil fuels.9 Renewables such as solar photovoltaics are expected to drop in price to below fossil-fuel generation prices in the next two to three years in most markets.10 Although any individual country may lack the optimal conditions for every type of renewable electricity, all countries are likely to have at least one or more options to produce electricity from renewables that will be cost comparative or cheaper than generation by fossil fuels.11

Figure 2: Levelized costs of electricity: renewables vs fossil fuel generation

This image illustrates the ‘Levelized costs of electricity: renewables vs fossil fuel generation.’

* Solar and wind include estimated costs to integrate 40% supply of intermittent power into electricity grids.

+ Fossil fuel power range includes health and environmental costs.

Data Source: IRENA

Externality costing will accelerate the shift to renewables

Electricity from renewable sources has significantly lower environmental impacts than from fossil fuels, most obviously on greenhouse gas emissions12 but on other variables as well such as air pollution and water use.13 Environmental externalities of fossil fuels are increasingly likely to be factored into the cost of their use14 and could lead to renewables becoming the technology of choice for almost all new capacity. Deployment rates for renewables are already very high in countries with an electricity shortage but could accelerate.15 Rapidly declining costs for storage16 and advances in demand and supply management17 could permit renewables to replace significant portions of the existing fossil-fueled electrical generation as power plants reach their end of useful life and are retired – both in emerging and developed economies.18

Renewables can reduce distribution infrastructure costs

Wind and photovoltaic power systems are highly scalable19 and distributable. They can provide power from the individual level through to utility scale and can be completely autonomous or fully integrated into electrical grids at local through to transnational scale. While grid- connected renewables will likely prevail in developed countries with existing grid infrastructure, the highly distributable nature of these renewables, combined with effective storage or load shifting, may permit countries with underdeveloped infrastructure to reduce costs of electrification by bypassing the traditional electrification pattern of extending grids from central power plants.20

Storage solutions are emerging and evolving faster than anticipated

An electricity-based ecosystem that incorporates significant solar and wind power will require storage to smooth the intermittent supply from these sources. This can be met by proven technologies like pumped hydro storage where conditions permit. While experience with renewables supply and demand management using integrated smart grids is growing, it is expected that energy-dense, low-cost batteries will be required for renewable-based electricity to dominate the global energy mix. Technologies in this area are emerging and evolving rapidly as researchers and companies work to meet the emerging demand for a wide range of battery applications, particularly in the power and transportation sectors.21 Simultaneously, costs are declining faster than forecasted.22 Tesla Motors is reported to be producing lithium ion batteries for the automotive and home energy23 markets at its Gigafactory24 for around US$300 per kWh – a price point that the International Energy Agency (IEA) predicted would not be reached until 2020.25 Battery manufacturers in Asia are building battery factories at similar scales to Tesla’s Gigafactory that will triple battery production by 2020.26 These economies of scale are expected to further reduce the cost of batteries to US$150 per kWh by 2020.27 At this price point, electric vehicles will become fully competitive with those powered by internal combustion engines. There is significant attention on lithium-ion technology and expanding the capacity and configurations of batteries using this chemistry. Research is also being conducted on other types of batteries such as sodium-ion or aluminum-air with the potential to substantially reduce the cost per kWh of manufacturing28 while improving energy density29, recharge performance and storage capacity. Further application of batteries is expected in a range of transportation modes including trains30, trucks31and even aircraft.32

Batteries are also likely to be widely deployed in stand-alone33 or grid-integrated photovoltaic and wind energy units to permit continuous power supply.34 Utility-scale energy storage technologies are available now and may be a cheaper alternative to peaking power plants as well as new transmission lines35 by allowing public utilities to position battery plants near high demand areas like large cities and industries and improve load-balancing while reducing GHG emissions. Battery manufacturers are developing different sizes of stationary battery units that store enough energy to power a single home or a factory and could be used by utilities.36 There is also potential to convert used lithium-ion batteries from electric vehicles into non-automotive applications like stationary storage units37 as the batteries still have significant energy storage capacity.

Tesla Powerwall (link is external)launch event on April 30, 2015.

(17:57 minutes)

Electricity’s flexibility allows it to cross energy silos and substitute for fossil fuels

Electricity is a versatile energy form which can be used efficiently for a variety of applications. Integrated energy production, storage and use systems are expected to develop in which electrical energy flow between uses will become more seamless and fluid.38 Systems thinking that focuses on shifting stored electrical energy between services as they are required (e.g. mobility, heat, light, computing) could allow electricity to become a fungible energy source across platforms that have traditionally been tied to a particular energy source (e.g. mobility using gasoline, building heat by natural gas, light and computing by electricity). Home owners may choose to charge their electric vehicles in off-peak hours and then connect the vehicle batteries into the home power system39 to act as a power source during peak demand hours. This type of multipurpose storage could dramatically increase efficiency of the overall energy system by shaving peak requirements and smoothing demand thereby accelerating the shift to intermittent renewables integrated with storage.

Data management will become a key element of the electrical energy system

The distributed and intermittent supply from some renewable power sources like wind and solar could add significant complexity to balancing supply and demand in electrical energy systems.40 Different business models will likely arise for integrating renewables into electrical systems depending on the degree to which a country already has an existing centralized power generation and distribution system. However, in all cases, intelligent energy management systems are expected to become more pervasive as increasing numbers of energy consumption and storage devices become connected in the Internet of Things.41 This could give rise to large integrated energy/data management companies that rival or replace government central utilities as the key actors in electrical energy systems.42

Heat from renewables could reduce demand for fossil fuels

Advances in technology could permit renewable sources to replace fossil fuels43 for much of the energy used for heating. Solar thermal can provide industrial hot water and steam in a temperature range of up to 400°C – warm enough to meet the demand from the textile, chemical, plastic, food and beverages and pulp and paper industries.44 Concentrated solar power can go higher.45 China leads the world in solar water heating capacity with 180.4 GWth46 and plans to increase its solar water heating capacity to 560 GWth by 2020.47 Solar heating technologies could be applied to supply hot water and space heating in the buildings sector thereby reducing the carbon footprint of the residential, commercial, and institutional sectors.48 Investments in transportation and distribution infrastructure for fossil fuel could be reduced or avoided if distributed solar thermal systems are widely adopted for space heating and processing heat.49 In addition, growth in demand for space heating (or cooling) may be lower than projected if robotics, remote control and automation remove humans from large parts of manufacturing and processing facilities or from mines to reduce the capital and operational costs of heating, cooling or ventilating.50

Renewables enhance national energy security, productivity and economic stability

Countries that do not have domestic supplies of a fossil fuel can increase their energy security and productivity while reducing economic risk by shifting their economies to renewable- generated electricity and heat. Most renewables can produce electricity and heat at lower cost than fossil fuels which makes economies that invest in renewables more competitive. Reducing the need for foreign supplies of coal, oil or gas reduces the requirements for political, military or economic geostrategic investments in fossil fuel rich regions as well as lowering the risks of price shocks if the flow of resources is interrupted.51

Some forms of distributed renewable energy like solar lead to greater overall employment and more locally-based employment than centralized power plants.52By providing inexpensive and reliable electricity close to the end use, decentralized renewables could create a feedback loop in which local economic activity evolves to take advantage of electricity, which will stimulate additional demand for electricity that will be met by additional supply by renewables.53

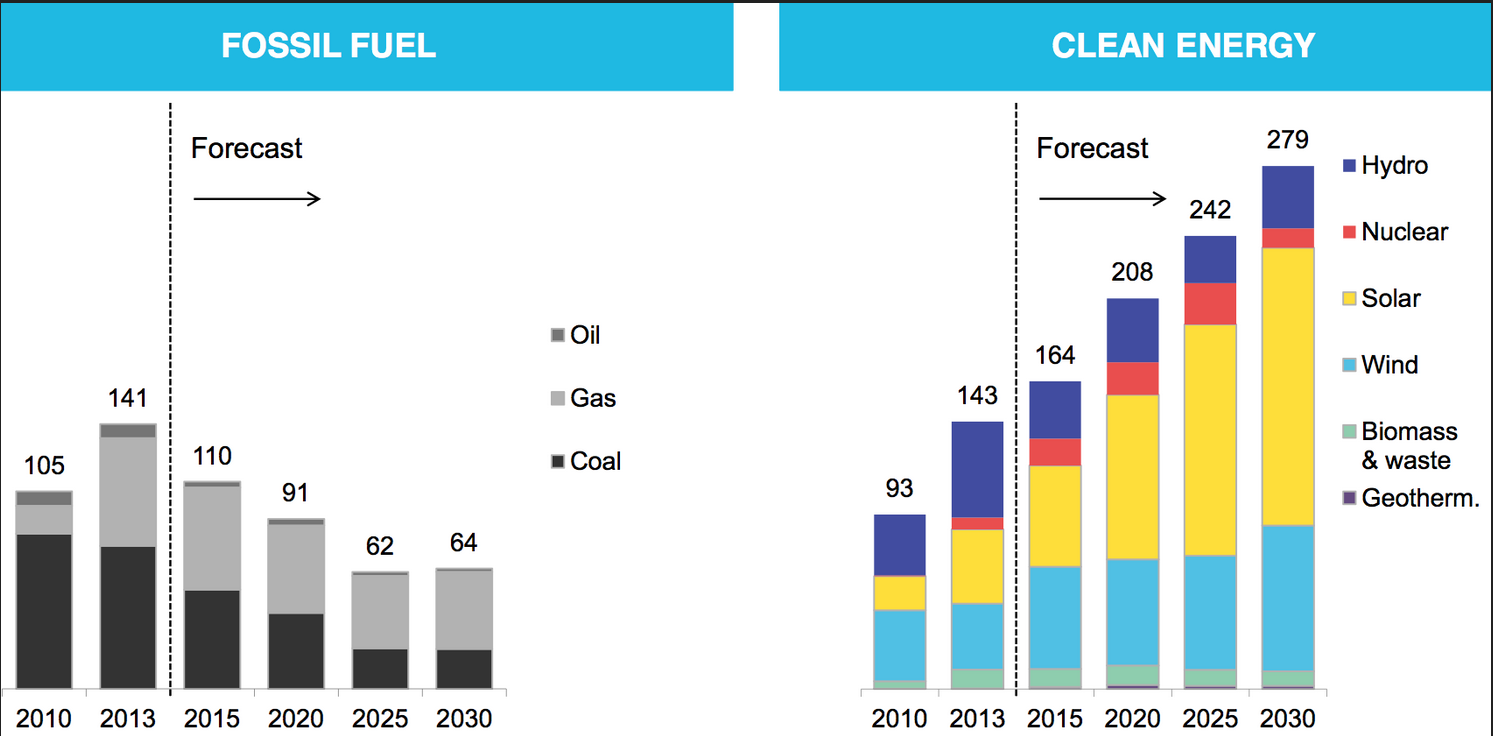

The increasing recognition of the multiple benefits of renewables compared to fossil fuel generation is reflected in Figure 3 which shows the global shift in the technologies being chosen to add electricity generating capacity. While significant investments in renewables are being made by national and state utilities and private utilities, many non-energy private sector companies also are directly investing in renewables as costs decrease and customers expect them to act on climate change. In search of energy self-sufficiency, IKEA has announced an investment of 500M euros in wind energy and 100M euros in solar energy for the next five years.54 Apple has announced a US$850M investment to build a 280 megawatt solar farm in California.55 Many companies listed in the Fortune 100 have adopted corporate renewable energy programs that scale up their use of on-site solar and wind power systems.56 To overcome some barriers with on-site power systems and meet their energy goals, 19 big brands representing a combined demand of more than 10 million megawatt hours per year or enough power to run 1 million homes for a year have signed last year the Corporate Energy Pledge, asking public utilities to make it simpler for them to buy power generated through solar, wind, fuel cells and other alternatives sources that are less subject to price fluctuations than fossil fuel.57 One of the objectives of the concerned companies is to have access to longer-term, fixed-price energy and renewables.

Figure 3: Power generation capactiy additions (GW)

This image illustrates the ‘Power generation capactiy additions (GW).’

Source: Bloomberg New Energy Finance

Transportation may electrify more rapidly than expected

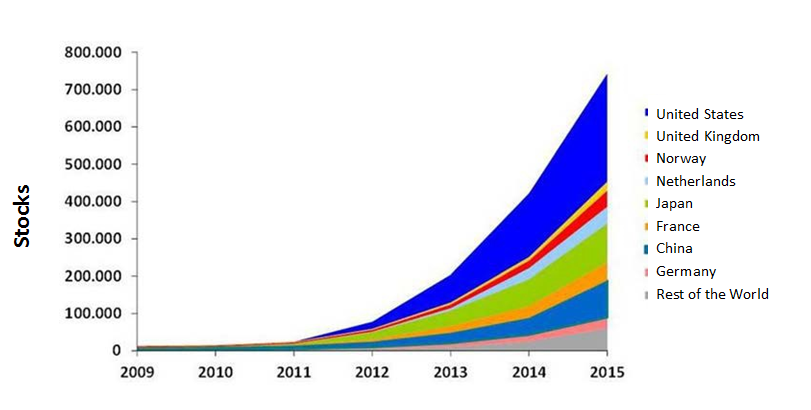

A number of factors could converge to shift a significant percentage of transportation to electricity over the next 15 years. The growth in electric vehicle sales shown in Figure 4 could accelerate, particularly in markets in which vehicle sales are expected to grow. Many of the countries making the greatest investment in adding renewables to the energy mix are the same ones facing the greatest regulatory pressures to reduce air pollution and greenhouse gas emissions as well as the highest projected demand for vehicles.58 Restrictions on vehicle purchases59 and incentives to purchase electric vehicles60 could accelerate their adoption in emerging markets. Potential declines in electric vehicle cost61 and increases in supply62 coupled with potentially lower than expected overall demand for personal vehicles due to emerging trends like car-sharing63 and telework64 could lead to a proportion of the global vehicle fleet that is more electrified than expected in many projections.65 66 A turnover of the vehicle fleet could occur much faster than historical averages if consumers and governments embrace autonomous vehicles for their enhanced safety and convenience.67 It is likely that those with the highest imported oil supply will shift to electrification of transport at the highest rate to reduce the risk of supply disruption or price volatility.68

Figure 4: Number of electric car sales by year and country

This image illustrates a graph representing the ‘Number of electric car sales by year and country.’

Source: Zentrum für Sonnenenergie- und Wasserstoff-Forschung Baden-Württemberg

Challenges and Opportunities

A new global energy ecosystem emerges rapidly

As electricity becomes more abundant, it may challenge fossil fuels in unexpected areas of transportation, processing, manufacturing and metallurgy which could previously only be performed technologically and affordably using fossil fuels.69 While the technical ability to generate renewable energy from wind and solar has been possible for decades, advances in technology and reductions in cost are permitting the globe to “discover” renewable-sourced electricity as a new energy source. Just as coal and then oil stimulated the development of technologies that used these energy sources, the emergence of cheap, reliable, abundant and non-polluting electricity combined with affordable energy-dense battery storage could accelerate the evolution of an electricity-based technological and industrial ecosystem that could out-compete and largely replace the current fossil-fuel based system.

Competition for emerging energy markets based on technology rather than resources

The assumption that regions such as Latin America or Africa will follow similar development paths to the West or even Asia and hence will be the next market for fossil fuels may be questionable. In an electricity-driven industrial and commercial ecosystem, emerging economies may leap-frog directly to renewable-generated electricity as the primary energy for their economic growth and development. Competition for these energy markets may be based on providing the best renewable energy technology and integrated energy efficiency/management systems rather than providing natural resources like fossil fuels. Those who develop the best technology would be the energy superpowers rather than those with the best oil, gas or coal deposits.

Minerals become strategic assets

Key minerals such as those required for batteries, photovoltaic cells and electric motors may replace petroleum as strategic energy-related assets. Latin America (Bolivia, Argentina and Chile) holds the largest lithium reserves in the world70 while China and Brazil have nearly 60% of the world’s reserves of rare earth metals.71 As storage and mobility become larger components of the electricity-powered ecosystem, there is potential for the creation of cartels or coordinated market manipulation for key minerals.72 This potential threat may spur countries to explore alternate battery chemistries that could further accelerate and expand the conversion to electricity by lowering cost and expanding options across sectors.73

Oil demand for transportation declines more rapidly than expected

A growing number of weak signals suggest a potential shortage of demand for fossil fuels rather than a shortage of supply. As electricity increases its proportion of the world’s primary energy supply and that energy is increasingly met with low-polluting, cost-competitive renewable generation, transportation could shift towards electrical power. Coupled with other factors that could reduce transportation demand (see Figure 5), demand for oil could peak sooner and decline faster than expected.

Figure 5: Future of asian oil demand

This graph is entitled “Future of Asian Oil Demand” and it suggests that Asia’s demands for fossil fuels could peak faster than expected in the next 10-15 years. The left side of the image is line chart with the x-axis representing the year 2015 and 2030 and the y-axis representing oil demand in millions of barrels per day.

Fossil fuels could lose their commodity status leading to splintering of the oil market

The assumption that fossil fuels such as oil are essential to drive economies may begin to be eroded as the availability of cost-competitive renewable-based energy increases and industrial and economic ecosystems embrace and evolve to use it. Grades of oil, natural gas and coal are largely considered uniform commodity products once they enter global markets. However, their sources vary significantly as can the geopolitical, environmental or social impacts of their extraction, production and transportation. If demand outstrips supply, discrimination between oil, coal or gas on the basis of these impacts may be limited, but if supply exceeds demand, pressure could mount to provide quantitative and qualitative information related to the source of the fossil fuel being sold. In this plausible future, the concept that coal, oil or gas is a globally uniform product could fail leading them to lose their commodity status.

If this were to occur, the global market for a fossil energy like oil could splinter into three broad tiers – the bottom (price only), middle (best mix of price but with floors on key criteria) and premium/high end (the purchaser will pay a premium to ensure all criteria are met). Embodied carbon in the production of the fossil fuel will likely be the first discriminator to be widely adopted. Others may follow such as associated environmental degradation; water consumption; air pollution; human rights record; indigenous inclusion; democratic freedom; inclusion of women; political and economic stability; lack of conflict; etc. If this were to come about, some fuels may have to sell at a steep discount to offset aspects of their production that are considered negatives by potential buyers. Rather than being price-takers from suppliers, consumer countries could become price-makers on different sources of oil as suppliers adjust pricing to maintain share of a diminishing and more discriminating market place.

Although oil is generally not segregated in the supply chain currently, increased data from sensors, big-data analytics and the Internet of Things could provide the information needed by purchasers at all points in the supply chain to more effectively track and discriminate between fossil fuel products from different sources. A system for open, transparent and verifiable tracking of oil from different sources and the products derived from them could be built using a Blockchain process. Similar programs are currently being developed to track the provenance of foods or other products from primary sources to end products.74 Alternately, fuel suppliers could emerge that only source their oil from suppliers meeting top tier criteria. Although the actual oil received by a purchaser may come from a pool of oil from all suppliers, the purchasers contracting from those suppliers would receive confirmation that top tier oil offset bottom tier oil in the pool and that the payment was directed to the producer of the top tier oil. This system would shift revenues from low tier producers to upper tier producers without disrupting a pooled oil handling system. This system would be similar to that used currently for “green power” from a provincial electricity grid.75 Delivered price could become only one of several characteristics used by purchasers of energy. It could be difficult to challenge these purchase decisions in the current multilateral trade regime as they would be made by individuals rather than at country level.

Scenarios

Scenarios are used to visualize how the future could evolve under different drivers and conditions. Scenarios are not attempts to predict the future, but rather to explore how the future might emerge, in order to test current assumptions and potential policy approaches against a range of alternatives.

Scenario 1: Resisting and reacting to change

- Canada continues a narrative that it has energy super power status based on its petroleum reserves. It continues to invest economic, social and political capital in expanding and maintaining production from the oil sands as a driver of employment, economic growth and tax/royalty revenues.

- Canada dismisses or actively resists domestic and international initiatives to encourage divestment in fossil fuels or to differentiate oil in international markets based on non- intrinsic qualitative measures.

- By defending the World Trade Organization rules that prevent discrimination of oil or petroleum based products based on their origin, and not taking steps to categorize oil based on non-intrinsic criteria, Canada is increasingly at risk of missing the expanding “premium” oil market and becoming a price taker. Needing to sell to the bottom of the market is further eroding investment in petroleum resources with impacts on tax and royalty revenues and employment. Its traditional market, the U.S., requires steep discounts on Canadian bitumen-derived oil as it needs to compensate purchasers for the downstream costs of emissions credits or carbon taxes that are imposed in the U.S., to permit it to meet the significant GHG reductions targets it accepted in negotiations with China.

- Negative perceptions on its climate/energy stance are spilling into non-energy related matters. Canada’s international “brand” is being significantly damaged and a wide range of Canadian products and services are considered “dirty” in the international market place.76 Soft power and influence continue to wane across a spectrum of issues.

- Significant financing costs for investments in fossil fuel infrastructure may need to be written off by the private sector or absorbed into government budgets at the taxpayer’s expense.

Scenario 2: Embracing and leading change

- Canada recognizes the growing importance of low-carbon energy as a key discriminator in a carbon-constrained global economy. It is expanding its already high electrification from renewable/non-emitting sources. Promoting its clean electricity story internationally is leading to its products and services being recognized and sought out for their low-carbon content.

- Canada is becoming increasingly adept at using its clean electricity by developing and/or being an early adopter of new technologies and processes in the expanding electricity- based industrial and commercial energy ecosystem. It is becoming an increasingly dominant global player in a number of key niche areas of electrical energy use such as data farming and mineral resource extraction/refining using new electricity-based processes.

- By taking a progressive role in developing and codifying the emerging international information base for the de-commodification of oil, Canada is positioning itself as an important player in this subset of the climate/energy issue.

- Shifting the component of Canada’s oil exports to premium (essentially conventional) sources is allowing it to retain and grow a share of the declining global oil market. Carbon Capture and Storage is cost effective due to advances in technology and environmental credits gained for recovering oil from existing conventional deposits.

- Research efforts continue on using the energy potential of the oil sands for alternate fuels through in situ biological transformation into hydrogen, ethanol and syngas which are used in transportation, chemicals, plastics and clean combustion to produce electricity for the U.S. Market.

Implications for Canada

Canada would be relatively well placed to take advantage of an electricity-based industrial ecosystem

Access to electricity is essentially universal in Canada77 and approximately 66% of the electricity it produces comes from renewable hydro power and non-greenhouse gas emitting nuclear power.78 This is in stark contrast to low electrification rates in many developing countries79 and to global electricity generation in which 75% is generated by fossil fuels. While significant parts of the world still need to add capacity and to shift to renewables, Canada has not only sufficient electricity for its domestic needs but capacity to export nearly 10% of its production.80 Canada also has significant potential to increase its total electricity production81 and to shift its electricity production further to low-carbon sources.82 These factors place Canada in an enviable position to export low-carbon electricity directly to markets in the U.S. and Mexico. Both economies could be expected to see increasing electricity demand while seeking to reduce their greenhouse gas emissions. The potential for long-distance transmission to further markets could increase as technology advances.83 Canada could also export technology, software and expertise in electrical energy production, particularly from hydro-electricity, as well as in electricity distribution, management, use and storage.

Data Centres: Economic Hubs of the Digital Economy

As digital technologies enable and penetrate more sectors of the global economy, electricity demand associated with data processing, storage and transmission is increasing both in absolute terms as well as share of end-use energy. Intercontinental exports of electricity are not yet cost-effective, but data can today be transferred efficiently between continents using high-speed fiber optic cables. Data centers can be located in areas with low-cost, low carbon electricity and favourable climates to reduce energy demand for cooling. Large, fast and reliable data centers could become innovation and economic hubs by attracting activities for which computational speed and/or volume are important. In an increasingly digital economy, benefits will come to those who are able to store, manipulate, transfer and apply data at the greatest speed and security and at the lowest cost and environmental impact.

Canada could become a global player in the emerging electrical industrial ecosystem in a number of ways. By hosting data centres, Canada could provide a significant share of the rapidly growing global electrical energy demand from the rising digital economy.84 As the economy becomes more digitally-based and additive manufacturing expands, many areas of production could be re-shored. Electricity could be exported to support similar re-shoring in the U.S. and Mexico. The cost competitiveness or preference for Canadian products or services produced with clean electrical energy could be increased in a carbon-constrained world. Canada could export low-carbon energy embodied in products or services85 by attracting production of goods or services that require a lot of electricity but are currently being produced in other countries using relatively high percentages of electricity generated using fossil fuels.

Canada could lead on research to switch industrial processes that are currently fossil-fueled to use electricity and/or be an early adopter of technologies developed elsewhere to produce low embodied-carbon products using electricity. Mineral processing and metallurgy are generally considered mature industrial sectors in which Canada may have a comparative advantage in developing or adopting disruptive technologies using electricity.86

Canada may hold many of the minerals and metals of an electrified digital world

As a new industrial ecosystem evolves to take advantage of electricity, the materials that are used in it will shift. New technologies will require greater amounts of minerals and metals such as lithium, graphite and cobalt for batteries as well as rare earths for the permanent magnets in electric motors.87 Canada’s well-developed exploration and mining expertise could place it in a relatively strong position to develop or partner with others to find and develop new sources.

Opportunities to find new applications for existing materials or to develop new bio-based materials could also be explored.

Canada may need to review the anticipated demand for its petroleum assets

A significant shift to electrification of personal transport combined with the potential slowing of demand for transportation of goods and people could result in oil demand peaking sooner and declining faster than forecast.88 If these trends were to continue, Canada may find that not all of its petroleum is marketable at prevailing prices, particularly if low-cost producers keep prices low by maintaining or even increasing supplies to keep market share and maximize the sale of their oil assets while oil still has economic value.89

Canada may need to reconsider the marketability of different types of oil reserves

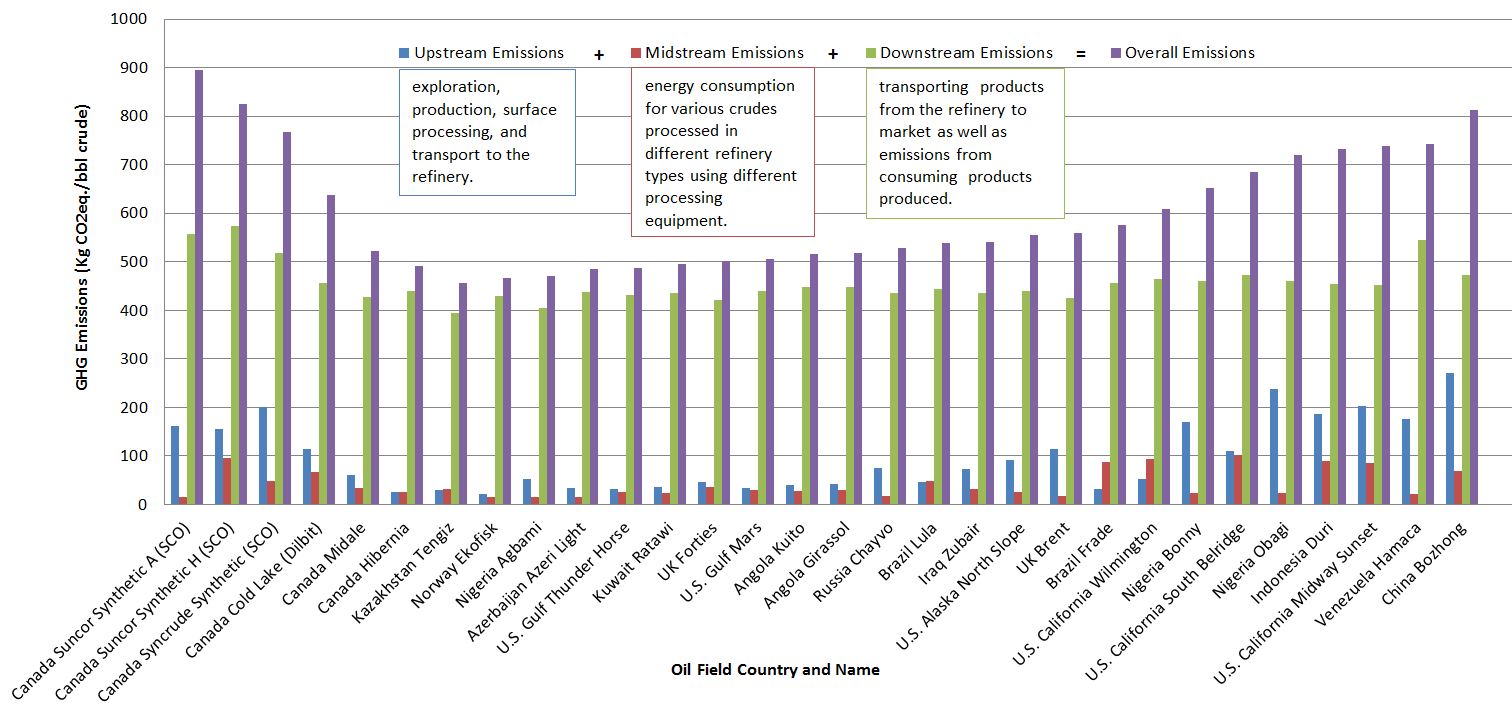

If global or regional markets for Canadian oil begin to differentiate oil based on non-intrinsic values such as embodied greenhouse gas emissions and splinter into tiers, Canadian producers could become either price-makers or price-takers depending on whether their reserves were rated as premium, middle ground, or low tier. It would be important for Canada to understand the criteria that are likely to emerge to define tiers and which of the deposits of fossil fuels in Canada could meet those criteria. As Figure 6 indicates, greenhouse gas emission metrics on some Canadian oil resources are lower than international reputation would suggest. Canada’s greenhouse gas emissions profile could be improved by selective development of oil sources even within oil sands deposits.

Figure 6: A comparison of greenhouse emissions: Canadian vs global oil fields

This image illustrates a graph representing ‘A comparison of greenhouse emissions: Canadian vs global oil fields.’

Source adapted from: Carnegie Endowment for International Peace, “Know Your Oil: Creating a Global Oil-Climate Index”, March 2015

The emergence of a rating system for deposits that classified them based on their tier could significantly reduce shareholder and company value if deposits are rated low or, conversely, increase shareholder value for companies with premium rated deposits. Potential spillover effects could be seen in stock markets like the TSX which are heavily weighted to resources like oil and from there into the economy as a whole.

Canada has a bulk handling system for oil, gas and coal but may have to consider source segregation, identification and certification for different tiers of oil to avoid rejection of low tier oil by a premium tier purchaser. If linked to a carbon pricing/tax scheme geared towards reducing carbon emissions, one could see a situation in which a purchaser could avoid paying carbon taxes or purchasing emissions permits by buying oil which already has a lower embodied-energy of production – the emission reduction would be considered to be intrinsic to the oil. Higher embodied-energy oil would sell at a discount because it would incur higher taxes or emissions permit costs when used.

Leading an orderly and responsible transition to a post-oil future

An emerging grid of actors opposed to oil production could be potentially very disruptive to the Canadian oil sector. The campaign to encourage investors to divest in fossil fuels90 may gain momentum. Recognizing that oil will still be a significant component of the global energy mix, at least in the near future, but that some oil is likely to remain in the ground, an opportunity may exist for Canada to demonstrate global leadership in an orderly and responsible transition to a post-oil future. If the market can choose amongst suppliers as a means to address climate change or other goals, it is likely that the demand will be greatest for the least environmentally or socially damaging oil. Canada may have oil that meets an emerging higher bar and by being active in this space, be able to bring this oil to market. An implication of tier- ranking is that some deposits may not be marketable and will have to be written off. This may require Canada to shift its thinking about where to invest in infrastructure and the tax/royalties streams that are likely from different types of oil deposits. There are also potential issues related to decommissioning stranded existing petroleum production and transportation infrastructure. Alternately, Canada may need to research and develop alternate uses for potentially stranded petroleum deposits or means to convert them into energy in forms other than oil such as methane or hydrogen.91 Use for plastics is not likely to be an option considering that no oil is used in plastic production in major markets like the U.S.92

Rethinking Arctic Development Strategy

There are potential implications for Canada’s Arctic if global oil and gas demand does not increase as expected. Arctic oil may be less marketable in an era of global oversupply because of its high cost (including embodied energy of production) but also high perceived environmental risk. Energy companies may be less interested in securing rights to oil and gas deposits in the Arctic or in the development of existing holdings which could reduce economic and employment opportunities for the region. However, materials such as minerals and metals needed in an electricity-based energy ecosystem or natural resources such as fisheries may emerge as assets with strategic and economic value. A shift away from oil and gas as an economic driver could require shifts in development and infrastructure investment decisions.

Low cost renewables could challenge Canadian power utilities’ business models

The potential for unsubsidized and decentralized renewables to produce electricity for the same (or lower) cost as traditional power plants may challenge Canadian utilities to provide cost-competitive electricity under the existing central utility model. In coming years, innovation, increased mass production capacities and market expansion of Asian, European and American companies will continue to drive down the cost of renewable energy devices and could undermine the competitiveness of Canadian central utility models.93

Canada may face multiple pressures to deregulate its electricity markets to permit greater penetration of renewable energy production and different business models for its distribution

The rapid expansion of renewables, particularly in Asia, may lead to new business models for electricity production and distribution based on the low-cost, scalability and decentralization of renewable energy. Renewable energy technology producers could look to expand their global share in foreign markets. Combined with the potential trade liberalization of environmental goods through the conclusion of the Environmental Goods Agreement94 within the World Trade Organization, foreign-made rooftop photovoltaic power or wind turbines and storage technology may become viable economic options for Canadian electricity consumers owning buildings in commercial, agriculture, institutional, governmental and industrial sectors. Consumers at the individual and corporate level may also drive a shift towards increased share of renewables, which may not be connected to the existing grid, based on their low cost and low carbon emissions.

The cost of electricity from central power plants may become more expensive95

In the Canadian system in which supply from provincially-owned centralized power plants already meets demand, additions of renewable energy from other actors will offset energy production from the central power plants. Costs of electricity from provincial utilities could increase because large scale nuclear and thermal power plants are optimized for continuous operation. Varying or reducing output from them can reduce their efficiency and increase their cost of operation. Provincial utilities also have debt servicing burdens to cover as well as significant costs associated with maintenance of extensive long-distance transmission lines that may not be required by decentralized renewable-based alternatives.96 Uncertainty about the time frame in which energy from decentralized renewable systems becomes cost-competitive with central utilities’ energy prices could increase the risk of public investments in state-owned power plants because the revenues from large, capital-intensive new power plants may not be sufficient to service the public debt incurred to build them.

Conclusion

It is increasingly plausible to foresee a future in which cheap renewable electricity becomes the world’s primary power source and fossil fuels are relegated to a minority status. This plausible future would seem to favour strategies that develop Canada’s own energy production and distribution systems to adopt and benefit from low cost renewable electricity. This would also provide Canada with the necessary expertise to participate in the growing global market for renewable powered electrification. By contrast, this plausible future would seem to recommend against long term investments in oil and gas production, refinement, and distribution infrastructure as these could be at high risk of becoming economically unviable as prices in renewable electricity further decline. At a minimum, this plausible future would suggest that governments ensure that the risks of further investments in oil and gas infrastructure be borne by private sector interests rather than taxpayers. Finally, while overall prospects for fossil fuel producers appear limited in this plausible future, there may be potential for some low-cost, low GHG-emitting Canadian producers to serve a niche market for green and ethical oil. Overall, the potential for significant disruptions in energy over the next 10-15 years, as illustrated in the plausible future described in this paper, would argue for caution by both governments and business to avoid long term investments that may not be viable under changing conditions.

Annex A: Assumptions

This foresight study challenges current assumptions about the expected future of the global energy landscape. It proposes alternative assumptions that are more likely to be robust across a range of future scenarios instead.

| Assumption | Robust Assumption |

|---|---|

| Fossil fuels will continue to dominate global primary energy supply. | Electricity will increase as a percentage of primary energy globally and may challenge fossil fuels as the predominant form of energy consumed in many economic sectors. |

| Renewable energy requires subsidies to be cost competitive with coal or natural gas powered generation. | Many types of renewable-based electricity generation are already cheaper without subsidies than generation by fossil fuel; those that are not are likely to be so within 10 years. |

| Environmental and social considerations will remain secondary to economics in energy supply and consumption decisions. | There may not be a requirement to incur environmental or social tradeoffs in increasing energy supply. Declining costs of renewable energy technology combined with increasing internalization of environmental and health costs of emissions from fossil fuels could make all forms of renewables the least expensive source of electricity within 10 years. |

| State-based centralized electricity utilities and extensive grids will continue to be the dominant business model for supply. | The scalability of renewables, particularly wind and solar could lead to regional or continental mega-grids that span multiple jurisdictions as well as to hyper-local or captive power that is not connected to a utility’s power grid. |

| The contribution of wind and solar to electricity generation will be limited by the high cost of storage needed to compensate for the variability of supply meaning that peaking plants will always be required. | Regional integration of wind and solar generation combined with advanced demand management can smooth intermittency significantly; storage may not be a limiting factor until wind and solar exceed 70% of supply; storage battery costs could continue to decline to be more cost effective than peaking plants; disseminated, internet-connected batteries in buildings and vehicles could act as virtual peaking plants. |

| Adoption rates for electric vehicles will remain low due to high upfront costs compared to internal combustion engine vehicles, short driving ranges and limited charging infrastructure. | Battery costs will decline to the point at which the drive-away cost of an electric vehicle is competitive with a conventional internal combustion engine vehicle; consumer experience with electric vehicles will reduce range anxiety; fleets may change over more quickly than historical average due to changing concepts of car ownership and regulatory measures to reduce environmental and health impacts of fossil fuel use. |

| Global demand for crude oil will substantially grow over the next 10-15 years, mainly driven by a rising vehicle market in emerging countries and growth in freight and aviation sectors. | Worldwide demand for fossil fuels could peak earlier and decline faster than predicted, leading to a softening of global demand. Emerging technologies such as electric vehicles and behavioural shifts such as virtual work and the sharing economy in the mobility industry may reduce the demand for oil for transportation. |

| Major oil producing countries will rebalance supplies to increase and stabilize prices. | Low-cost oil producers may not curtail supply in order to maintain their share of a diminishing market, seeking to maximize the extraction of their reserves before oil is replaced as a predominant energy source. |

| Petroleum-based fuels and products are commodity goods. | Purchasers at all points in the supply chain may be able to track products produced from different sources of oil and discriminate between those products based on intrinsic qualities of the source oil as well as non- intrinsic qualities such environmental or social impacts of extraction, transportation and production of the products. |

References

1 IEA, World Energy Outlook 2014(link is external), Executive Summary.

2 IEA, World Final Consumption (2013)(link is external). Electricity’s share in industry’s total final energy consumption almost doubled from 15 % in 1973 to 27 % in 2012.

3 IEA, World Energy Outlook 2014 Factsheet(link is external).

4 IEA, World Energy Outlook 2014 Factsheet(link is external).

5 Energy Research Institute, National Development and Reform Commission, China 2050 High Renewable Energy Penetration Scenario and Roadmap Study(link is external), 2015.

6 Centre for Energy-Efficient Telecommunications, University of Melbourne, The Power of the Wireless Cloud(link is external). The CEET models estimate the 2012 wireless cloud energy consumption at 9.2 Terawatt hours. The estimated energy consumption of the wireless cloud for 2015 is between 32 Terawatt hours and 43 Terawatt hours – and increase of between 390% and 460% over three years.

7 Policy Horizons Canada. 2015. Energy Cluster Findings – The Future of Asia: Implications for Canada.

8 REN21, Renewables 2014: Global Status Report, 2014, p 21; IEA, Renewables information, 2014, Paris, OECD publications.

9 IRENA, Renewable Power generation costs in 2014(link is external), 2015.

“January 13, 2015, “Unsubsidized rooftop solar electricity costs anywhere between $0.13 and $0.23/kWh today, well below retail price of electricity in many markets globally. The economics of solar have improved significantly due to the reduction in solar panel costs, financing costs and balance of system costs. We expect solar system costs to decrease 5-15% annually over the next 3+ years which could result in grid parity within ~50% of the target markets. If global electricity prices were to increase at 3% per year and cost reduction occurred at 5-15% CAGR, solar would achieve grid parity in an additional ~30% of target markets globally. We believe the cumulative incremental total available market for solar is currently around ~140GW/year and could potentially increase to ~260GW/year over the next 5 years as solar achieves grid parity in more markets globally and electric capacity needs increase”

Clean Technica, « Solar Pv Costs to Fall Another 25% in Three Years »(link is external), May 26 2015.

MIT, The Future of Solar Energy: An Interdisciplinary MIT Study(link is external), May 2015, p.127.

11 IRENA, Studies on Renewable Energy Potential(link is external).

12 Wikipedia, Life-cycle greenhouse-gas emissions of energy sources(link is external), 2015.

13 World Resources Institute, Identifying the Global Coal Industry’s Water Risks(link is external), April 2014.

World Resources Institute, Water Risk Atlas.

World Resources Institute, Shale Resources and Water Risks(link is external).

The Globe and Mail, High-tech environmental push needed for oil sands: Tory-requested report(link is external), May 2015.

14 World Bank, State and Trends of Carbon Pricing, 2014.

15 John A. Mathews et Hao Tan, Economics: Manufacture renewables to build energy security, Nature, vol. 513, no 7617, September 10, 2014; IEA, World energy outlook, 2014, p. 235; IRENA, Installed Renewable Power Capacity – Cumulative capacity, for China, Japan, India, Malaysia, Thailand(link is external).

16 Björn Nykvist et Måns Nilsson, Rapidly falling costs of battery packs for electric vehicles, March 2015. “We show that industry-wide cost estimates declined by approximately 14% annually between 2007 and 2014, from above US$1,000 per kWh to around US$410 per kWh, and that the cost of battery packs used by market-leading BEV manufacturers are even lower, at US$300 per kWh, and has declined by 8% annually. Learning rate, the cost reduction following a cumulative doubling of production, is found to be between 6 and 9%, in line with earlier studies on vehicle battery technology2. We reveal that the costs of Li-ion battery packs continue to decline and that the costs among market leaders are much lower than previously reported. This has significant implications for the assumptions used when modelling future energy and transport systems and permits an optimistic outlook for BEVs contributing to low- carbon transport.”

Tesla, Powerwall(link is external) : La batterie domestique de Tesla.

17 GE, Wind in the Cloud? How the digital Wind Farm will Make Wind Power 20% More Efficient(link is external), May 2015.

IBM, IBM Research Launches Project “Green Horizon”’ to Help China Deliver on Ambitious Energy and Environment Goals(link is external), July 2014.

18 Global Research, « Replacing Fossil Fuel and Nuclear Power with Renewable Energy: Wind, Solar and Hydro Power »(link is external), March 2014.

Bloomberg, Obama’s EPA Rule is Redrawing the U.S. Coal Map(link is external), April 2015.

19 Brookings, Making Renewable Power Sustainable in India(link is external), January 2015.

20 RMI, Learning from the Cell Phone Phenomenon: How Microgrids Can Help Developing Countries Leapfrog into a New Energy Paradigm(link is external), July 2013.

21 S.C. Mueller, P.G. Sandner et I.M. Welpe, « Monitoring innovation in electrochemical energy storage technologies: a patent-based approach », Applied Energy, 2014. DOI : 10.1016/j.apenergy.2014.06.082.

22 IEA, Global EV Outlook: Understanding the Electric Vehicle Landscape to 2020, 2013, p. 17.

23 Tesla Motors, Powerwall(link is external)

24 Tesla Motors, Gigafactory Tesla(link is external).

25 Björn Nykvist et Måns Nilsson, Rapidly falling costs of battery packs for electric vehicles(link is external), Nature, March 2015.

26 Tesla, Planned 2020 Gigafactory Production Exceeds 2013 Global Production(link is external)

Reuters, China’s BYD takes aim at Tesla in battery factory race(link is external), March 13 2015.

27 Morgan Stanley, Solar Power and Energy Storage: Policy factors vs. Improving Economics(link is external), July 28, 2014, p. 6.

28 ECN, Design to improve material properties of sodium-ion batteries(link is external), June 26, 2015.

NextBigFuture, « Sakti could mass produce next generation solid state battery for around $100 per kwh »(link is external), March 26, 2015.

29 Fortune, Tesla’s gigafactory could be obsolete before it even opens. Here’s why(link is external), April 27, 2015.

30 The Guardian, Low carbon battery-powered train carries first passengers(link is external), January 13, 2015.

31 570News, Tesla Motors co-founder Ian Wright wants to electrify gas-guzzling commercial trucks(link is external), June 2, 2015.

32 L’OBS Economie, « L’E-Fan d’Airbus, premier avion 100% électrique à traverser la Manche »(link is external), July 10, 2015.

33 Green Mountain Power, Tesla Powerwall(link is external), 2015

34 Mark Chediak et Dana Hall, Elon Musk says utilities shouldn’t fear his battery systems(link is external), Bloomberg, June 8, 2015.

35 Reneweconomy, « Graph of the Day : Myth of cheap shale gas and cheap energy »(link is external), January 14, 2015.

36Tesla Energy(link is external)

Daimler, Sales Launch of private energy storage plants(link is external), June 9, 2015.

37 Charged, Nissan, GM and Toyota repurpose used EV batteries for stationary storage(link is external), June 17, 2015

Gizmag, « Nissan to incorporate used Leaf batteries in stationary energy storage system »(link is external), June 15, 2015.

38 Nissan Motor Corporation, Vehicle to Home Electricity Supply System(link is external).

39 Nissan, Leaf to Home Electricity Supply System(link is external). Automobile propre, « Smart-grid – Nissan expériemente le « leaf to home » au Japon »(link is external), December 2014.

40 Institute for Energy Research, Germany’s Electricity Market Out of Balance(link is external), August 2014.

Eric Martinot, How is Germany Integrating and Balancing Renewable Energy Today?(link is external), January 2015.

41 Bloomberg, China out-spends the US for first time in $15bn smart grid market(link is external), February 2014.

GSMA, How China is set for global M2M Leadership(link is external)June 2014.

Owen Poindexter, The Internet of Things with Thrive on Energy Efficiency(link is external) FutureStructure, July 28, 2014.

Youtube, Smart Energy Systems: 100% Renewable Energy at a National Level(link is external)November 2014.

YouTube, Smart Solar Energy Management with SMA(link is external), February 2015. (it’s not the best video but it show something quite interesting, home smart system able to accede to weather forecast could tell when is the best time to use appliances and as appliances are becoming smart well it could start the washing machine without you at the right time);

Youtube, What is the Smart Grid?(link is external), June 2013.

42 IBM, Smart Grid(link is external).

Tesla, Powerwall: Powerwall Tesla Home Battery(link is external).

Breaking Energy, New Storage Technologies Open Doors for Wind and Solar(link is external), May 2015.

43 IRENA, Solar Heat technology for industrial process – potential, 2015, p. 4, “approximately 40 % of industrial primary energy consumption is covered by natural gas and approximately 41 % by petroleum“(link is external).

44 IRENA, Solar Heat technology for industrial process – potential(link is external), 2015.

45 American Institute of Chemical Engineering, Molten Salt Gives Concentrated Solar a Unique Advantage(link is external);

The bright future of solar thermal powered factories(link is external).

YouTube, Melting steel with solar power(link is external), 2008.

46 IRENA, Solar Heat technology for industrial process – potential(link is external), 2015.

47 Solar Heat World Wide, Markets and Contribution to the Energy supply 2012(link is external), 2014.

IEA, Technology roadmap: Solar Heating and Cooling, 2012, p. 26.

48Drake Landing Community(link is external).

Drake Landing Community. “The Drake Landing Solar Community (DLSC) is a master planned neighbourhood in the Town of Okotoks, Alberta, Canada that has successfully integrated Canadian energy efficient technologies with a renewable, unlimited energy source – the sun. The first of its kind in North America, DLSC is heated by a district system designed to store abundant solar energy underground during the summer months and distribute the energy to each home for space heating needs during winter months. The system is unprecedented in the World, fulfilling ninety percent of each home’s space heating requirements from solar energy and resulting in less dependency on limited fossil fuels. The Government of Canada and its Canadian industry partners are proud to showcase Canadian solar thermal and energy efficient technologies in this one-of-a-kind community”

49 The Economist, LNG: A Liquid market(link is external), 2012.

50 RIA, Robotics and Energy Cost Reduction, 2006. “Because robots can operate unsupervised, they can produce items while people are not present. The ability to operate in the dark or in unheated environments can lead to substantial energy savings on the part of manufacturers.”(link is external).

51 Business Insider, China has crossed a major investment threshold that is going to change the entire world(link is external), February 2015.

52 IRENA, Renewable Energy and Jobs: Annual Review 2015(link is external), 2015.

UKERC, Low Carbon jobs: The evidence for net job creation from policy support for energy efficiency and renewable energy(link is external), November 2014.

53 Kenichi Imai, Impacts of Electrification with Renewable Energies on Local Economies: The Case of India’s Rural Areas(link is external), March 2013.

54 Le Monde, Ikea s’engage sur les énergies renouvelables(link is external), June 2015.

55 Ecowatch, Tim Cook: New Solar Farm Will Be Apple’s ‘Biggest, Boldest and Most Ambitious Project Ever(link is external), February 2015.

56 Renewable Energy World, Big Companies, Big Renewable Investments, August 2014.

57 WWF, Powering Businesses on Renewable Energy(link is external).

GreenBiz, Apple, Ikea, Walmart : 12 leaders in on-site renewables(link is external), December 2014.

58 Skolkovo, Emerging Markets Transforming the Global Automotive Industry(link is external).

“By 2030, China’s annual sales are expected to reach 39 million, or 28 percent of global sales. India’s motor vehicle market will be powered by both rapid increases in population and per capita income, giving it the fastest growing market for motor vehicle sales over the next two decades”.

59 World Resources Institute, 4 Lessons from Beijing and Shanghai Show How China’s Cities Can Curb Car Congestion(link is external).

60 China Business Review, Opportunities and Challenges in China’s Electric Vehicle Market(link is external), February 2015.

61 Björn Nykvist et Måns Nilsson, Rapidly falling costs of battery packs for electric vehicles(link is external), March 2015; Clean Technica, BYD Gigafactories to Rival Tesla and Panasonic(link is external), March 2015.

62 Pinar De Neve, Electric Vehicles in China(link is external), June 2014.

Environment News Service, Electric Cars Key to India’s Energy and Climate Security(link is external), May 2014.

63 Nextgov, Autonomous cars will destroy millions of jobs and reshape US economy by 2025, May 14, 2015.

64 Karen Hickey, « What the world thinks of telecommuting », June 12, 2013; David Hill, U.S. Being Left In The Dust Of The Global Telecommuting Revolution, SingularityHUB, February 21, 2012.

65 BP, Energy outlook 2035(link is external), 2015, p. 34.

ExxonMobil, The Outlook for Energy: A View to 2040(link is external), 2015, p. 17 et 18.

Agence internationale de l’énergie, World Energy Outlook 2014(link is external), 2014.

66 The Globe and Mail, Does Stretching out a car loan make financial sense?(link is external), July 6, 2015.

67 Brookings, Autonomous vehicles will have tremendous impacts on government revenue(link is external), July 7, 2015.

Nextgov, Autonomous cars will destroy millions of jobs and reshape US economy by 2025(link is external), May 14, 2015.

68 International Business Times, Electric Cars Would Lower UK Oil Imports By 40%, But Only with Much Wider Adoption(link is external), March 2015.

Cambridge Econometrics, Fuelling Britain’s Future, March 2015, p. 56.

69 Solar Impulse(link is external). et Wikipedia ; Solar Implusle(link is external).

M. Gebler, et al. A global sustainability perspective on 3D printing technologies(link is external),

Energy Policy, novembre 2014, p. 158-167;

M. Kreiger, et. al., Environmental Life Cycle Analysis of Distributed Three-Dimensional Printing and Conventional Manufacturing of Polymer Products(link is external),

ACS Sustainable Chem. Eng., vol. 1, no 12, p. 1511; H. Yoon, et al., A comparison of energy consumption in bulk forming, subtractive, and additive processes: Review and case study(link is external), International Journal of Precision Engineering and M’anufacturing-Green Technology, July 2014.

70 GreenTechmedia, Is there Enough Lithium to Maintain the Growth of the Lithium-Ion Battery Market?(link is external), June 2, 2015.

71 Statista, Rare earth reserves worldwide as of 2014(link is external), by coutry.

72 Greentechmedia, The Geopolitics of Lithium Production(link is external), June 30, 2015.

73 Greentechmedia, The Geopolitics of Lithium Production(link is external), June 30, 2015.

Will Latin America Become the New Middle East?(link is external), May 2012.

Erik Bethel, Is Lithium the 21st Century’s Oil?(link is external), 2010.

74 Reid Williams, How Bitcoin’s Technology Could Make Supply Chains More Transparent (link is external), CoinDesk, May 31, 2015.

75 Bullfrog Power: Supporting green energy the easy way(link is external).

76 TerraEco, « Le CO2 importé plombe la facture »(link is external), 2015.

77 Access to electricity (% of population)(link is external), The World Bank.

78 Canada Balance, IEA, 2012. Note that other sources place this figure higher – see “Acting on Climate Change” reference below.

79 Access to electricity (% of population); op. cit.

80 Canada Balance, 2012, op. cit.

81 About Renewable Energy(link is external), Natural Resources Canada.

“According to a study commissioned by the Canadian Hydropower Association, there is a significant amount of undeveloped technical hydropower potential in all provinces and territories: 163,173 MW, more than double the existing capacity. Technical potential refers to possible hydropower capacity without considering factors such as economic feasibility, Aboriginal rights, or environmental impacts.”

82 Acting on Climate Change, Solutions from Canadian Scholars(link is external), 2015. “Seventy-seven percent of Canada’s electricity is already produced from low-carbon emission sources. Combining current hydroelectric production capacity with plentiful untapped renewable energy resources and east-west intelligent grid connections between provinces, could allow Canada to adopt a target of 100 percent low-carbon electricity production by 2035.”

83 PennEnergy, Siemens wins major HVDC order to connect British and Belgian power grid(link is external), June 2015.

Power Engineering International, China Takes HVDC to New Level(link is external), June 2013.

YouTube, ABB enables Europe’s longest HVDC link: NordLink(link is external), March 2015.

YouTube, ABB Launches world’s most powerful extruded HVDC cable system(link is external), 2014.

YouTube, Shaping the power grid with HVDC solutions(link is external), June 2014.

Power-Technology, The World’s longest power transmission lines(link is external), February 2014. et their crowdfunding project(link is external).

84 Greenpeace, Clicking Clean: How Companies are Creating the Green Internet(link is external), April 2014.

85 TerraEco, Le CO2 importé plombe la facture(link is external), 2015.

Low-Tech Magazine, How Sustainable is stored Sunlight?(link is external), May 2015. 86 Kevin Bullis, New Titanium-Making Process Could Result in Lighter Aircraft(link is external), MIT Technology Review, February 26, 2015.

87 Allianz, Materials used to make a car infographic(link is external).

MadeHow, Electric Automobile(link is external).

BBC, The Electric car’s biggest threat may be its battery(link is external), March 2014.

The market Oracle, Electric Cars Materials and Resources Demand(link is external), February 2010.

88 Energy Cluster Paper, Policy Horizons Canada, 2015.

89 Christophe McGlade and Paul Ekins, The geographical distribution of fossil fuels unused when limiting global warming to 2° C, Nature, vol. 517, 2015;

Andrew Leach, Are oil sands incompatible with action on climate change?(link is external), Maclean’s, Jeff Lewis, Is oil sand development still worth it?(link is external), October 28, 2014.

The profitability and viability of liquefied natural gas projects in Canada may depend on high natural gas prices in Asia, Andrew Nikiforuk, « Tanking Asia Gas Prices Makes BC LNG Not Viable, expert says »(link is external), The Tyee, January 15, 2015.

90 Fossil Free, Divest from Fossil Fuels(link is external).

91 University of Calgary, The Optimized System for Carboxylic Acid Remediation (OSCAR)(link is external), IGEM 2012.

92 U.S. Energy Information Administration, Frequently Asked Questions, How much oil is used to make plastic?

93 John A. Mathews et Hao Tan. Economics: Manufacture renewables to build energy security, Nature, vol. 513, no 7617, September 10, 2014.

94 WTO, Joint Statement regarding the launch of the environmental goods agreement negotiations, July 2014.

95 Rocky Mountain Institute, The Economics of Load Defection: How grid-connected solar-plus- battery systems will compete with traditional electric service, why it matters, and possible paths forward(link is external), 2015.

96 CleanTechnica, This Graph Dispells The Myth That Cheap Gas Means Cheap Energy(link is external), January 2015.